Energy Market Insight | February 2024

Energy Market Trends: FEBRUARY 2024

PRICES ACROSS THE CURVE CONTINUE TO FALL AMID STRONG SUPPLY PICTURE

WHAT IMPACTED ENERGY PRICES IN FEBRUARY 2024?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Mild temperatures throughout February curb demand

- Gas prices were close to 3-year lows

- Oil markets remain range bound despite Middle Eastern concerns persisting

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

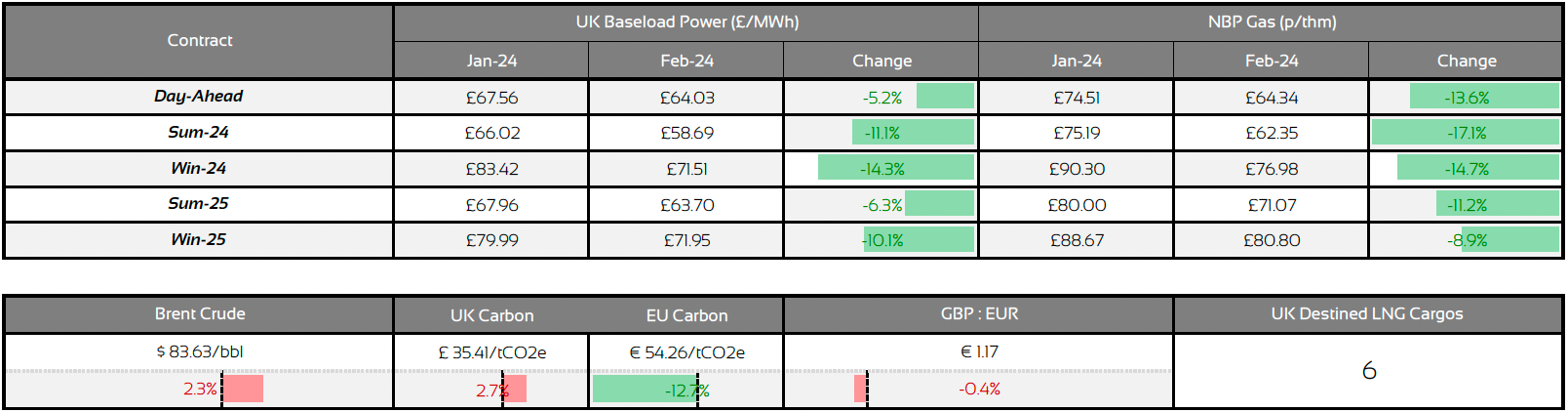

Day Ahead GAS & POWER Prices

UK Temperature CHANGE

UK Gas Demand - Gigawatt hours (GWh)

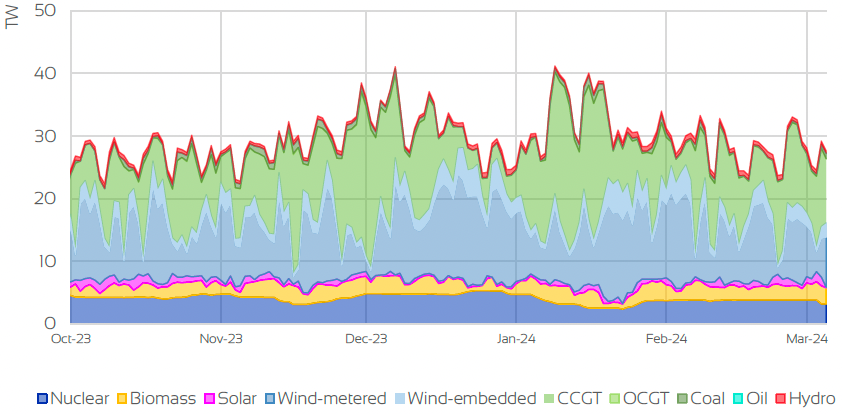

UK GAS SUPPLY MIX

Market Insight: Short-Term

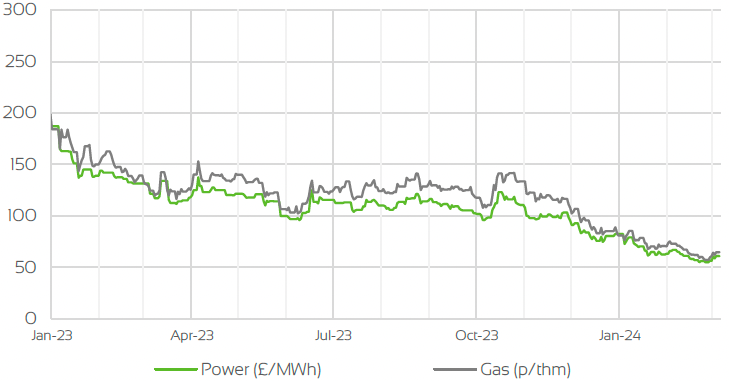

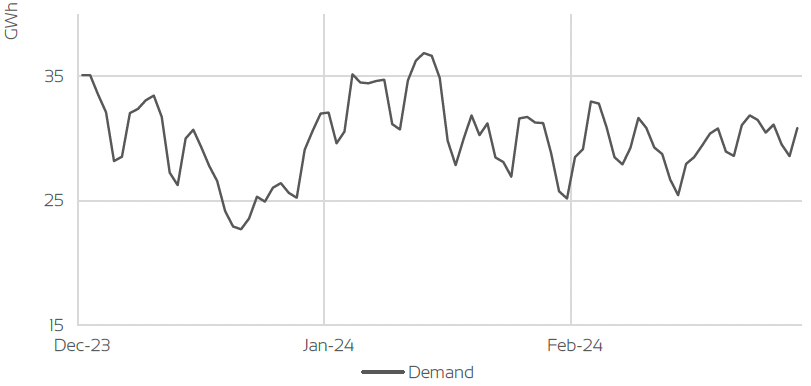

Gas and power contracts across the curve continued where they left off in January and saw significant losses throughout February. As the summer months drew closer and demand for this time of the year were particularly low, the supply fundamentals remained unchanged amid ample gas inventories and solid gas supplies via Norwegian pipeline flows and LNG imports.

The threat of the war in the Middle East disrupting LNG supplies had somewhat faded despite ongoing military action in the Red Sea, as U.S and UK forces countered Houthi attacks on commercial shipments. Despite this causing some delays to LNG cargoes from countries such as Qatar, ample imports from America still resumed, keeping LNG stock comfortable throughout February.

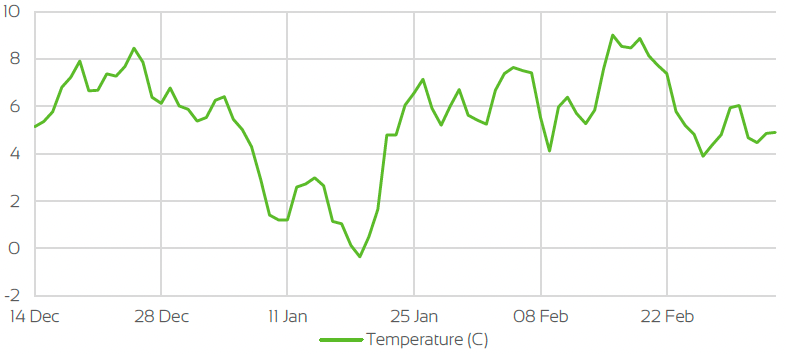

This in turn supported gas prices falling, as they came close to a 3-year low, with prompt and seasonal index’s dipping below the 60p/Therm mark. Gas prices did however retreat and edged over the 60p/Therm come March due to technical buying and some support from unplanned Norwegian outages. Power prices faired in similar fashion as prompt and seasonal markets dropped below the £60/MWh mark as temperatures for the majority of the month hovered above norms curbing demand, which was also supported by stable wind generation throughout the month, lowering gas demand for power (CCGT). With gas storage across Northwest Europe remaining high and at similar levels to the previous 2 years, the outlook come the end of the winter looks very comfortable.

Capacity throughout the month was still above the 62% mark as the month ended, and with withdrawals kept relatively low, the outlook for March will remain bearish in the short-term at least. Despite Norwegian gas flows remaining stable overall throughout the month, some bullishness had crept into the market amid some small, unexpected outages, but the impact on markets were kept at a minimum and if anything restricted any further losses.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

Front Seasonal gas & power Prices

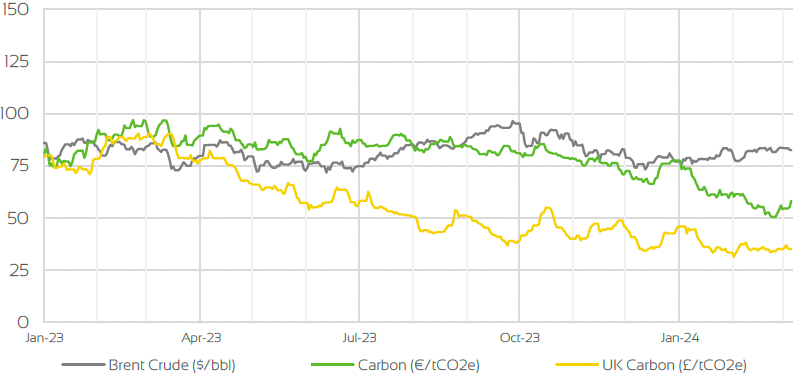

Brent Crude & Carbon Price

UK, EU & US Currencies

Coal Prices

Market Insight: Long-Term

As the majority of the winter has seen a significant downwards trend amid milder temperatures and healthy gas inventories, the outlook for the Q2 & Q3 will remain largely bearish for the time being. As gas inventories remain high, the summer months will be a period of recovery to prepare for the winter months come October. With storage expected to be still around the 50% mark as we move into April, injections won’t be as aggressive as previous years due to comfortable level of gas. With that said, the long-term geopolitical concerns will still be apparent as the war in Israel is still ongoing, and any potential ceasefire looks to be off the books at the moment, despite attempts from the U.S to bring fighting to a halt.

The escalation of the conflict in the Red Sea is also a reminder that possibilities of the war spreading is still apparent which could still hinder supplies further down the line. But with demand from Asia seemingly on slight decline and exports from the U.S still strong, the impact could be minimal (LNG). Further out on the commodity complex, has seen oil prices remain relatively rangebound throughout the month, despite the ongoing geopolitical risks. The attacks from Houthi rebels has added a lot of the bullish sentiment in Brent/Crude markets, but demand concerns have limited further gains, as weak economic data from large importers such as China and further delays on interest rate cuts in the U.S continue push back on gains.

Therefore leaving prices hovering above the $80/Bbl mark for the majority of the month. The IEA (International Energy Agency) had initially forecasted 2024 to be a year of increased demand despite faltering economies, but recent suggestions of OPEC+ looking to make further production cuts could be an indicator that demand is still not where it is expected to be.

Market Outlook

As markets across both the gas and power curves show significant losses throughout the winter period, with February being no exception, the outlook is likely to remain bearish as a whole. With gas prices heading close to 3-year lows, the supply outlook for the remainder of the winter looks extremely comfortable, especially with ample storage which is current sitting above the 62% mark.

With recent unplanned outages at some Norwegian plants which added some upside into contracts, this is likely to be one of the few risks that will have any meaningful impact on markets for both the prompt and seasonal curves in the short-term. Though with that said, nominations overall have still been strong for the majority of 2024 and is likely to stay that way for the rest of the winter period.

Wider risks from the Middle East will still be a concern as LNG shipments may still be impacted with delays, and with no clear view on when this will end, concerns will still be evident. With that said, supplies of LNG coupled with Norwegian gas flows continued to be robust, and with steady wind generation, the supply picture going into the summer months will remain comfortable. Therefore, it is still apparent that there is still room for further downside.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.