Energy Market Insight | January 2024

Energy Market Trends: JANUARY 2024

START OF 2024 REMAINS BEARISH OVERALL, BUT GEOPOLITICAL TENSIONS CONTINUE

WHAT IMPACTED ENERGY PRICES IN JANUARY 2024?

TOP 3 FACTORS AFFECTING ENERGY PRICES

- Strong supply picture & mild temperatures continue to weigh on contracts

- Fears of the war spreading in the Middle East persists

- Oil prices rise in January as Red Sea attacks adds bullishness

WHAT ARE THE SHORT-TERM ENERGY PRICE IMPACTS?

Short-Term ENERGY MARKET TRENDS & INDICATORS

Day Ahead GAS & POWER Prices

UK Temperature CHANGE

UK Gas Demand - Gigawatt hours (GWh)

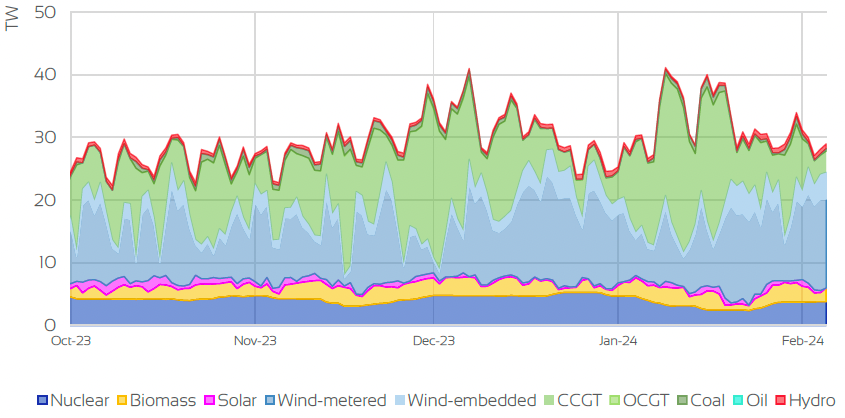

UK GAS SUPPLY MIX

Market Insight: Short-Term

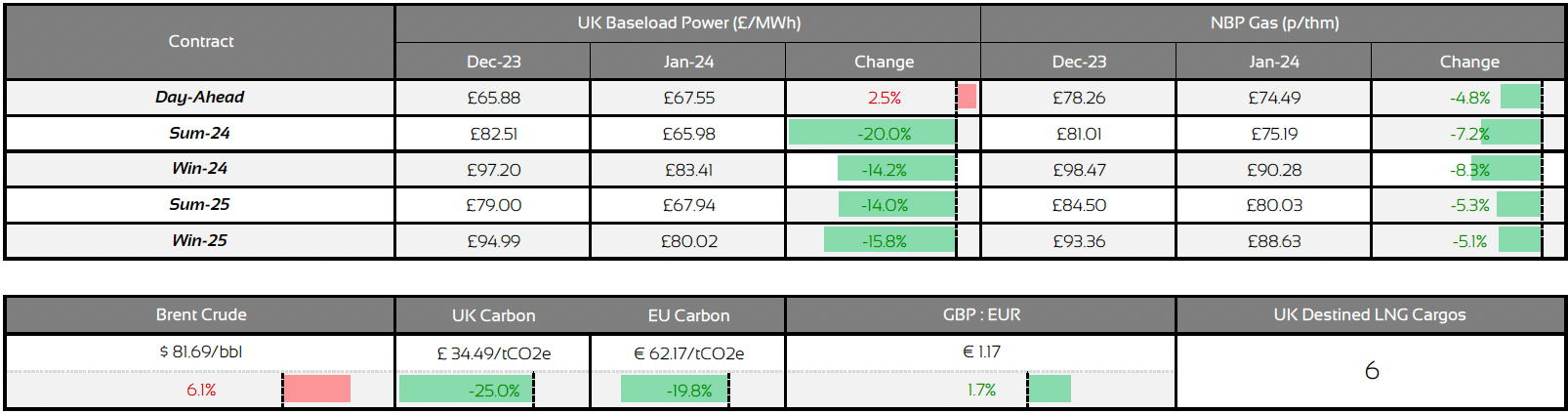

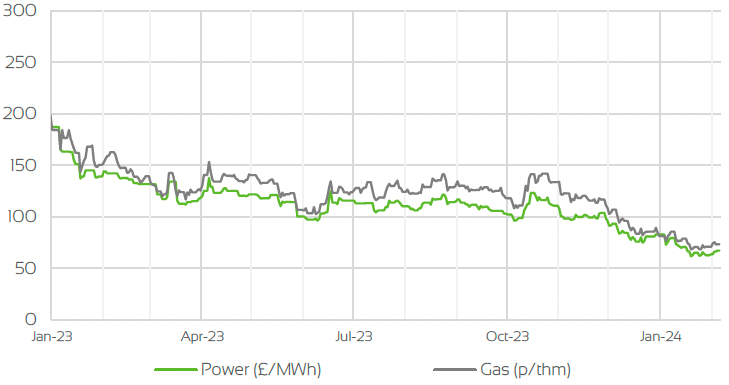

The start of 2024 has seen little change in terms of direction as January continued to see a steady decline in contracts, not only across prompt indexes but also across the seasonal curves. A comfortable supply picture along with mild temperatures for the majority of the month has again been a significant factor in which markets have been trending. Wider geopolitical factors have in some form limited any further downside, as the war in Israel remains a concern, coupled with tensions at the Red Sea, as the militant group Houthi maintain intermittent attacks on cargo’s passing through.

This has led to the US and UK retaliating, stoking fears of the war spreading and disrupting the flow of LNG & oil respectively. With that said, Prompt markets across both gas and power have remained in a bearish trend throughout the month as near curve power prices sit comfortably between the £60-£69/MWh mark with prompt gas prices hovering just above 70p/Therm.

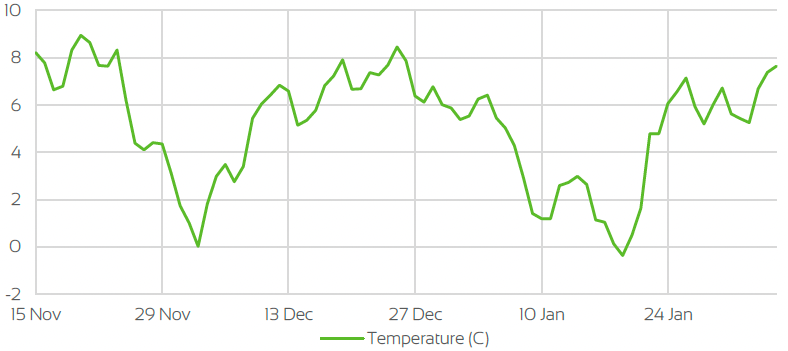

Gas storage levels across Northwest Europe have been slowly declining but at large are extremely comfortable, as capacity was still above 70% fulness, and despite some concerns of delays for LNG cargo from the Middle East, imports have continued to be strong throughout the month. Therefore, analysts are forecasting inventory levels in Northwest Europe come summer-24, being above the 50% mark. Temperatures throughout January overall have been generally at norms or above compared to previous years and with forecasts of further milder conditions in February, the short-term outlook will stay bearish for the time being.

Pipeline gas flows from Norway have again been strong throughout the month with little maintenance/outages impacting nominations to Europe and the UK, and with wind generation also strong overall throughout the month, the supply fundamentals remain unchanged.

WHAT ARE THE LONG-TERM ENERGY PRICE IMPACTS ?

LONG-Term ENERGY MARKET TRENDS & INDICATORS

Front Seasonal gas & power Prices

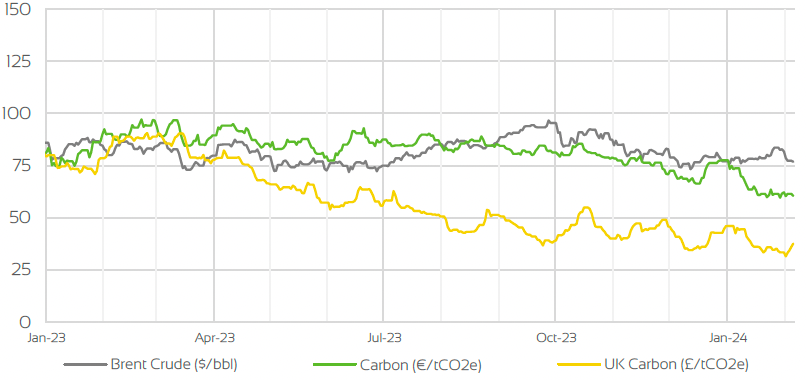

Brent Crude & Carbon Price

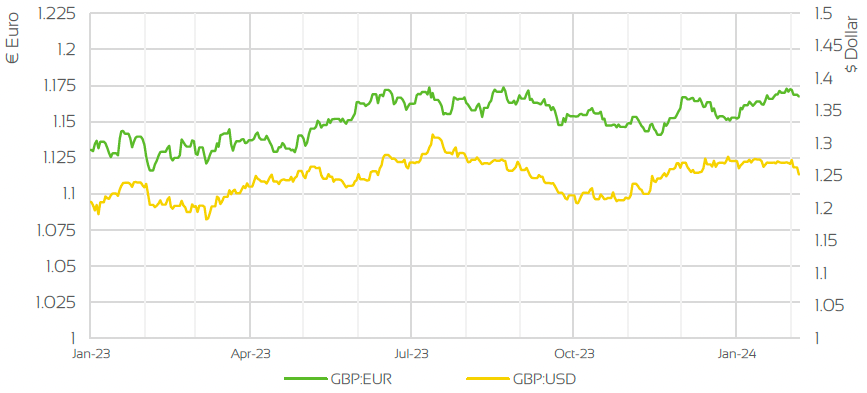

UK, EU & US Currencies

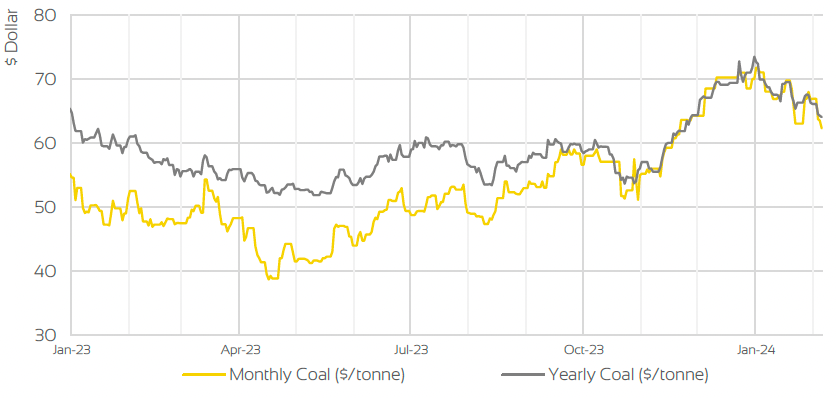

Coal Prices

Market Insight: Long-Term

As we move closer to the summer months and start preparing for winter-24, gas storage levels and temperature forecasts become more impactful on markets prices, but with gas inventories likely to be above the 50% mark as we near April, the long-term outlook is likely to remain relatively bearish. Seasonal contracts for both gas and power faired in a similar trend to prompt prices with Summer and Winter-24 markets falling as a strong supply picture throughout the winter months continue to weigh on markets further out.

As it currently stands, the war in the Middle East has had little impact on prices but concerns still persist. Fears of the war spreading will still be largely apparent, especially with latest tensions at the Red Sea, as both LNG and Oil shipments re-route around Africa in order to complete deliveries. Qatari officials have already notified some European nations of delays on LNG due to re-routing, but as exports from the U.S and Norwegian pipeline flows continue to be robust, the outlook currently will not be a concern for the upcoming winter-24 period. The continuation of war and fears of it spreading will still be present and is likely to limit losses in the longer term despite the supply outlook being in a strong position moving into the summer months.

Oil markets throughout the month have been somewhat bullish due to the ongoing tensions in the Middle East, as prices saw a monthly gain as they moved above the $80/Bbl mark. Fears of supply disruptions, coupled with ongoing production cuts from OPEC+ and expectations of demand increasing this year added much of bullishness into prices. Though with concerns still persisting with current demand levels and economic recovery from major nations, any further gains would have been limited.

Market Outlook

The start of Q1 has seen losses throughout the month in January, which is a continuation of what we have experienced throughout winter-23. The strong supply picture, mild temperatures and comfortable gas inventories has continued to weigh on prices across the curve. With most of the supply fundamentals not really changing, the EU and UK are set to leave the current winter period in a very strong position, as long demand forecasts remain as expected.

As per the concerns in December amid the ongoing war in the Middle East and with it escalating to the Red Sea, fears of the conflict spreading is unlikely to shift in the mid to short-term at least as the war seems far from over. Bullish sentiment is likely to persist, which will limit losses overall amid the strong supply picture.

The knock-on effect of the war in Israel could impact LNG and oil supplies globally, but it has not yet shown much driving force amongst European gas and power markets as of yet but should not be taken lightly if delays in LNG shipments persist in the long term. With that said, LNG from the Middle East is still robust and with gas storage levels in Europe still strong the market outlook is still strongly in favour of being bearish, especially as we head into February.

Related News

EXPLORE OUR OTHER ENERGY MARKET INSIGHTS

BOOK YOUR 30-MINUTE ENERGY MANAGEMENT CONSULTATION

Fill in your details below to arrange a complimentary consultation with one of our experts. They will give you bespoke advice to help your business achieve all its energy needs, reducing cost, consumption and carbon.